Poultry valuation tables: introduction

Updated 6 July 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at /government/publications/poultry-valuation-tables/poultry-valuation-tables-introduction

The government has powers to cull (kill) animals to control the spread of some animal diseases.

For bird flu and Newcastle disease, you’ll get compensation for any healthy birds that are culled by the government. Read guidance on compensation for certain diseases in poultry and other captive birds.

The Animal and Plant Health Agency (APHA) uses poultry valuation tables (or specialist valuers for specialist stock) to determine compensation for poultry culled. These tables are produced for the APHA by the agricultural and environmental consultancy, ADAS.

Poultry valuation tables are reviewed and updated regularly to ensure that they reflect current costs for different types of birds and different production systems. Normally, these reviews are undertaken quarterly, with new tables being issued late in March, June, September and December each year. Due to the recent volatility in production costs and the number of avian influenza cases in Great Britain, these timings have been changed to include updates in November and January, rather than in December.

The current valuation tables are based on costs and other information gathered in June 2026.

Types of poultry included

The poultry valuation tables include information about:

- broilers

- laying hens

- turkeys

- ducks and geese

- game birds (pheasants, partridges and mallards)

The tables also include information about production systems, such as indoor, free range and organic.

Data sources

Numerous sources are used to gather data on current costs. These include published information as well as intelligence provided confidentially by a range of different industry stakeholders, such as feed compounders, breed companies, suppliers of fuels and other materials and poultry producers. Where possible for each cost item, information is gathered from a range of different sources, so that overall sector trends can be established.

Data summary

Since the last update in March, compound feed prices have generally increased for most poultry, although there have been some reductions in certain sectors.

Turkey poult prices have been reviewed for the 2026 Christmas growing season and these have been adjusted accordingly in the tables. A change has been made to the tables for slow-growing birds (indoor, free range and organic) in that the earliest age at which these turkeys are assumed to be marketable has been reduced from 15 to 13 weeks. This reflects increased demand for smaller carcasses and breeding developments.

There has been an increase in the cost of day-old broiler chicks and for pullets in the egg sector. Energy costs have generally increased but prices are currently volatile and subject to change.

Next update

The next update is scheduled for the end of September 2026.

Contact

For further information, email Mailys.Chezaud@adas.co.uk

ADAS

June 2026.

Methodologies used in developing the poultry valuation tables

How the tables are calculated

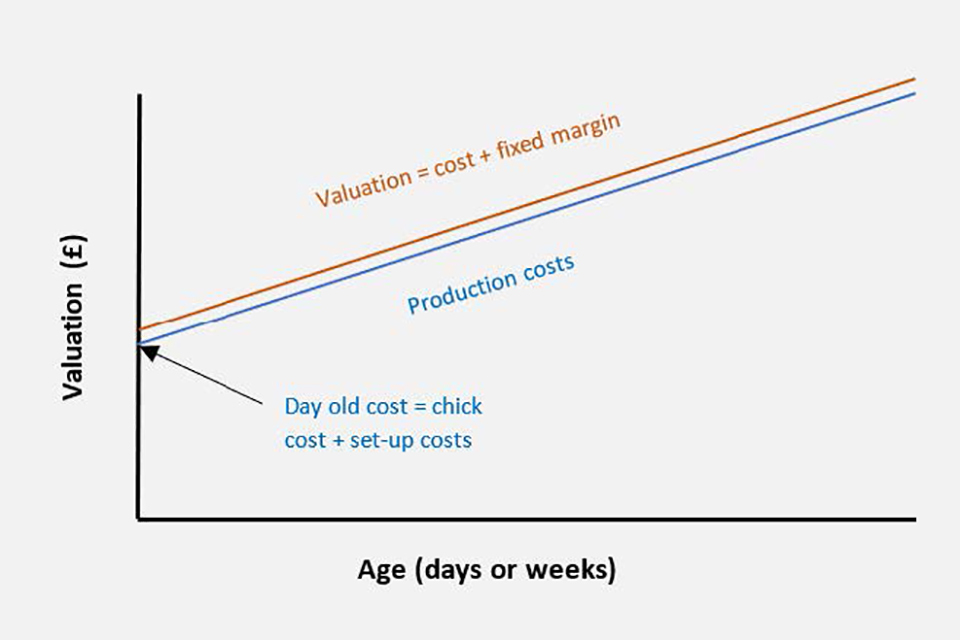

For most table poultry species and for rearing birds, the valuation at each flock age is calculated from the costs incurred for a typical flock, to that point. Throughout the production cycle, a small fixed financial margin is added to the production costs to reflect notional market value and this is indicated by the higher of the two lines. (Figure 1). Costs at the time of stocking are derived from the cost of the chick or poult and the house ‘set-up’ costs.

Figure 1. Valuation principles for table birds and replacement layers

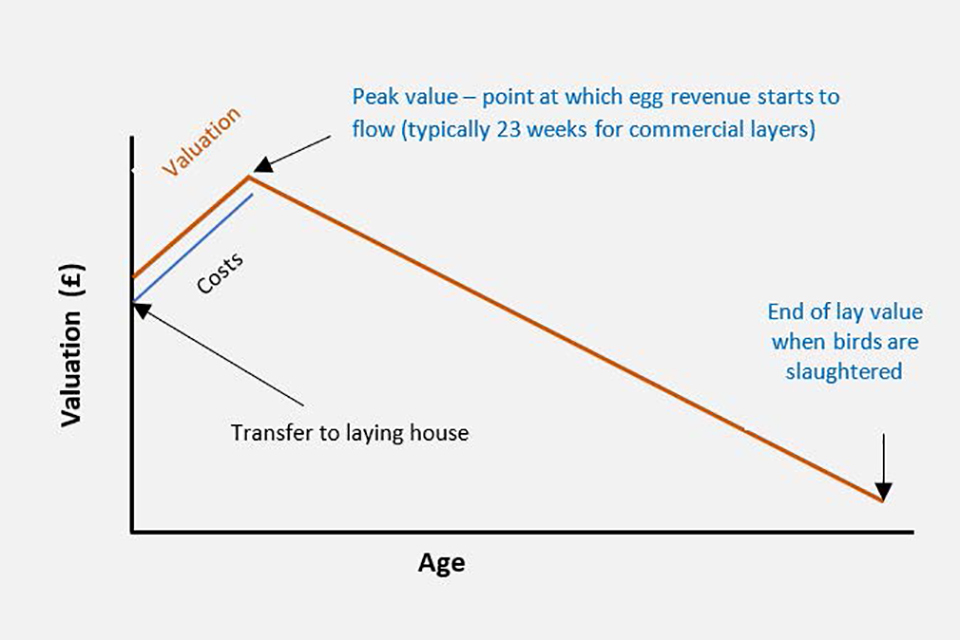

For egg laying flocks, valuations are based on typical costs incurred and the expected final value of the bird at the time of depopulation. After transfer to the laying house, the valuation rises to a peak value when egg revenue begins to flow. From this point, the value of the bird is depreciated on a straight-line basis to the expected end-of-lay value (Figure 2).

Figure 2. Valuation principles for egg laying birds

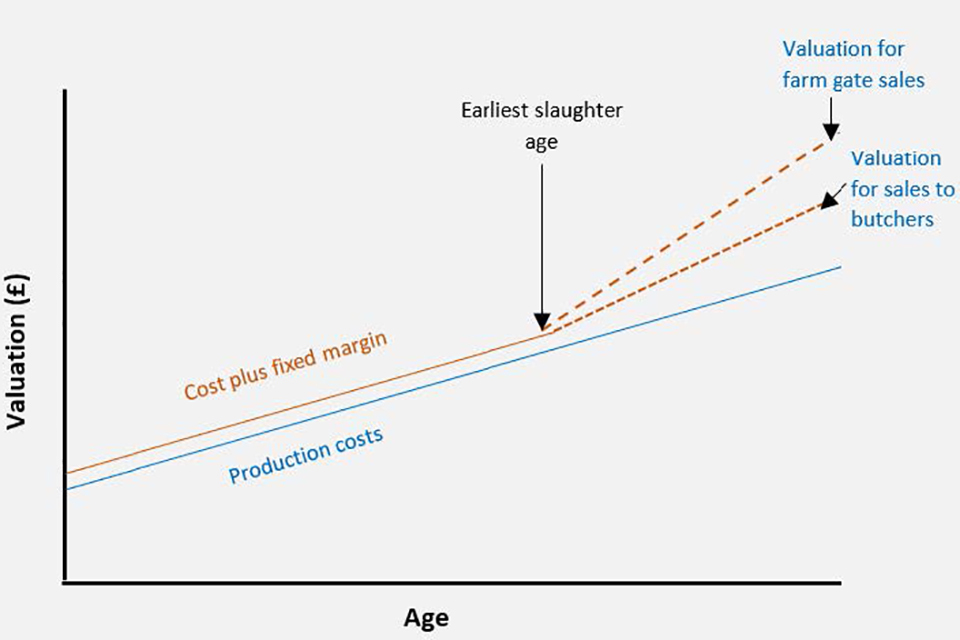

Some table bird enterprises (for example, geese and seasonal turkey production) attain a very high market value at normal slaughter ages relative to their costs of production. In order to address this issue and arrive at valuations that are fair and reasonable for this type of enterprise, valuation principles have been developed that are based on costs of production (with a fixed margin) up to the point at which the birds can normally be marketed. Once the birds are at an age when they are mature enough to be slaughtered and offered for sale through regular channels, the valuations are based on expected marketing method (to butchers or farm gate sales) and typical sales price, less slaughter, processing and distribution costs (Figure 3).

Figure 3. Valuation principles for high value birds